Over the course of 2013, many factors might have been expected to lead to a slowdown in Asian dollar bond issuance. First of all, interest rates have risen from their lows in 2012, with the yields on 10-year Treasuries higher by over 100bp. While everyone knew that interest rates had to normalize at some point, the rise in yields brought that fear to the front and center of everyone’s thinking. Then, in May, Bernanke raised the possibility of slowly withdrawing the monetary accommodation with his discussion of “tapering.” Third, for the last three weeks, we have tried to grapple with the possibility that the U.S. government may have to cut back on paying for its commitments and expenses if the debt ceiling is not raised by October 17.

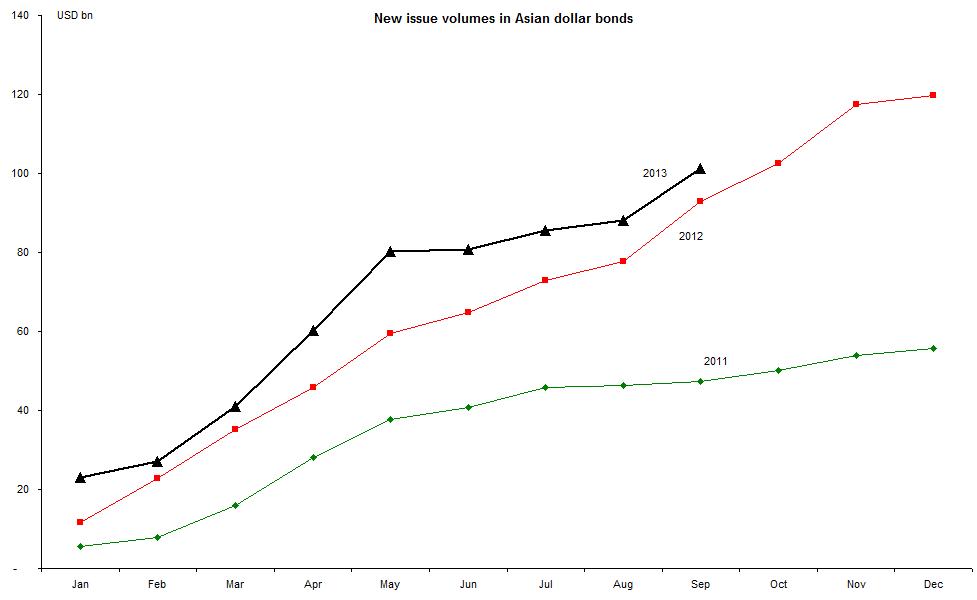

In the midst of all this, Asian bond markets have had a great year in terms of new issues. So far this year, by our count, over USD 110bn worth of dollar-denominated bonds have been issued by Asian issuers. Month after month, in terms of issue volumes, 2013 has outpaced 2012 (which itself was a record year).

In the midst of all this, Asian bond markets have had a great year in terms of new issues. So far this year, by our count, over USD 110bn worth of dollar-denominated bonds have been issued by Asian issuers. Month after month, in terms of issue volumes, 2013 has outpaced 2012 (which itself was a record year).

It must be noted that this year’s record volumes are despite the lean period in June to August, when only USD 7bn was issued in the full three months. Although this period is usually a low season, this year’s volume was much below the USD 18bn issued during the same three months last year.

What accounts for the robust state of this market? Are investors blithely indifferent to the ructions around them?

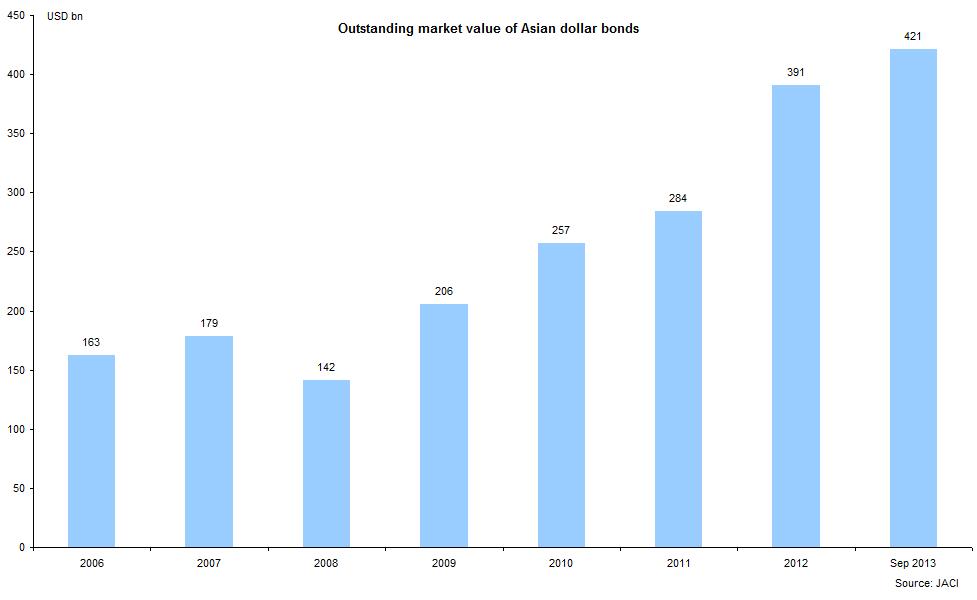

The first thing to recognize is that much of the new issues are simply replacement for maturing bonds. This becomes clear if we consider the increase in the net market value outstanding at the end of the last few years (see chart below). This year, the market value has risen by USD 30bn – not a bad number, but still a slower pace of growth.

What accounts for the robust state of this market? Are investors blithely indifferent to the ructions around them?

The first thing to recognize is that much of the new issues are simply replacement for maturing bonds. This becomes clear if we consider the increase in the net market value outstanding at the end of the last few years (see chart below). This year, the market value has risen by USD 30bn – not a bad number, but still a slower pace of growth.

The figures nevertheless show that net new money has been available for bond issues, despite the repeated challenges. From the issuers’ point of view, the cost of funding is still attractive. Yields of 2.6% on 10-year Treasuries are still near the multi-decade lows, and the bond spreads are also reasonable although higher than the pre-crisis levels. From the investors’ point of view, Asian dollar bonds still offer a pick-up over comparable US domestic issues, even among investment-grade bonds.

At this stage, it is fair to say that Asian dollar bonds have become a legitimate, large asset class with a diversified pool of issuers and sufficient liquidity for investors. Asian dollar bonds represent roughly 40% of all emerging market dollar bonds. Even as interest rates continue their upward journey in the medium term, we believe that institutional money would still be actively engaged in this market.

At this stage, it is fair to say that Asian dollar bonds have become a legitimate, large asset class with a diversified pool of issuers and sufficient liquidity for investors. Asian dollar bonds represent roughly 40% of all emerging market dollar bonds. Even as interest rates continue their upward journey in the medium term, we believe that institutional money would still be actively engaged in this market.

RSS Feed

RSS Feed