This is the reproduction of an article in IFR Asia.

To many global investors, bonds from China’s property sector are toxic nuclear waste, not to be touched at any cost. To others, they come with a more pragmatic “handle with care” warning. I belong to the latter camp.

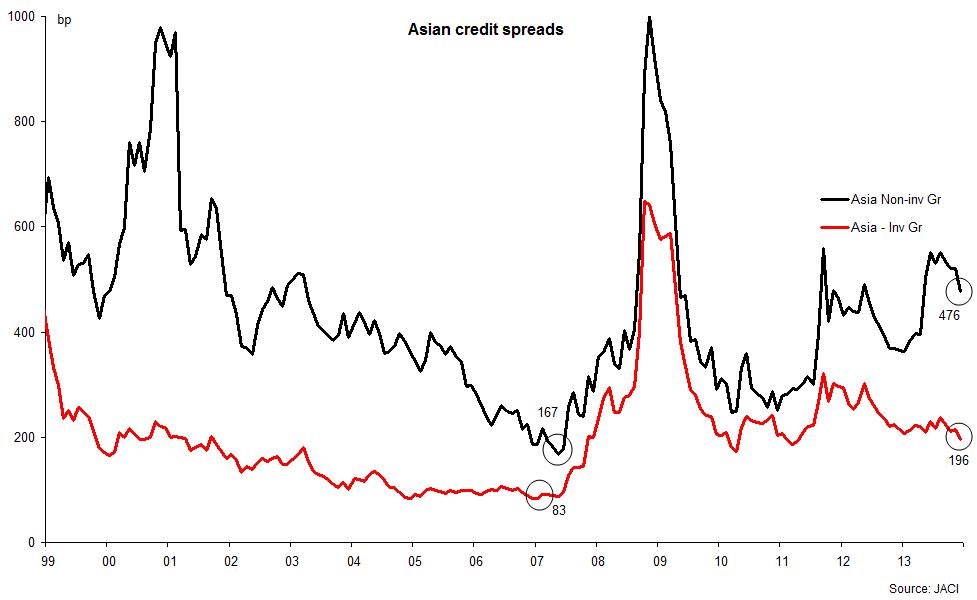

From just a handful of bonds 10 years ago, the sector has grown to contribute 9.5% of the Asian US dollar bond market with US$51bn of bonds trading. That is nearly a third of all high-yield corporate bonds in the region.

Over this period, the sector has gone through three cycles of downturns and upturns. Several Chinese property companies have issued, redeemed and refinanced their offshore bonds. Companies with credit ratings ranging from Single A to Triple C have managed to issue bonds, which trade actively in the secondary market. Yet, a feeling of unease persists.

Perhaps the first source of discomfort is the fact that offshore Chinese property bonds are deeply subordinated, since they are issued by offshore-incorporated entities, which inject the bond proceeds as equity into their onshore companies and service their debt only out of equity dividends received back from the mainland. The difficulties in repatriating equity funds out of China mean that the offshore principal effectively has to be refinanced. In case of bankruptcy, the onshore lenders have the first claim over the onshore assets.

While this structural weakness is undoubtedly true, it applies to every other bond issued by Chinese businesses, including investment-grade bonds far beyond the property sector, since the structure was born out of regulations prohibiting the issuance of debt or guarantees by mainland companies. (Only recently have the authorities begun to relax this prohibition, and the first few offshore bonds are now coming out with direct guarantees from mainland operating companies.)

ANOTHER SOURCE OF discomfort is the government’s meddling in the property sector through various measures, including the flow of credit to the builders, rules for financing land purchases, obtaining mortgages, and mortgage down-payment requirements. The harshest controls came in 2010 when the government restricted the number of apartments that an individual could purchase.

Property prices are a sensitive subject everywhere, and China is no exception. The government presses the brakes if the prices are speeding too fast and pushes the accelerator if property construction flags too much so as to threaten the overall economic growth.

This government intervention makes asset values volatile in both equity and debt markets, and raises the cost of capital to the sector.

Some investors have also been scared away by stories of oversupply and ghost cities. The property development business model, by definition, consists of a long operating cycle, and there may be genuine demand/supply imbalances, as in any other industry, but the overwhelming majority of Chinese properties are built in response to actual demand from a rapidly urbanising population. The same goes for talk of speculative buying, when the reality is that most of the properties are bought for self-occupation. Buyers have to put up a minimum 30% down-payment, they are not over-leveraged and there is no subprime lending.

WHEN IT COMES to investing in Chinese property bonds, one should realise that there has already been one level of filtering – only those companies large enough to go through a rating process and the expense of issuing offshore actually end up selling dollar bonds. They are all listed offshore, most of them in Hong Kong, and are subject to audits and disclosures that go with the listing status. The additional scrutiny from equity analysts and investors that comes with listing also offers additional information for bond investors.

There has not been a single default in the sector so far, and only two distressed exchanges in 2009, both at 80 cents to the dollar. Some companies did go through financial distress during previous sector downturns, but they managed to sell land or unfinished projects to stronger players and stave off default.

This is not to argue that we would never see a default in the sector. We will, sooner or later. But the sector has genuine fundamentals, strong and weak players, and saleable assets that can be realised in times of distress.

So, how should one approach investments in Chinese property bonds? First of all, investors need to be prepared for the volatility that comes with the regulatory changes. Any crash in value following a regulatory tightening offers an opportunity to pick up the higher-quality bonds at more attractive prices. In fact, such moves also enable the stronger players to buy out the weaker ones or to acquire assets from the struggling players, and increase their market share.

The current downturn in the market is no different. It is true that the stock of unsold property is running above average; that the leverage has increased in the last 12-18 months in response to slowing sales; that margins are under pressure due to the pressure to liquidate stock; and that some of the weaker companies are likely to experience a liquidity crunch in the next 12-18 months, unless they slow down their expansion. But the current downturn is also an opportunity to pick up bonds issued by stronger companies, which will benefit from the tight conditions in the sector. The challenge is reading the credit fundamentals carefully enough to identify the winners.

From just a handful of bonds 10 years ago, the sector has grown to contribute 9.5% of the Asian US dollar bond market with US$51bn of bonds trading. That is nearly a third of all high-yield corporate bonds in the region.

Over this period, the sector has gone through three cycles of downturns and upturns. Several Chinese property companies have issued, redeemed and refinanced their offshore bonds. Companies with credit ratings ranging from Single A to Triple C have managed to issue bonds, which trade actively in the secondary market. Yet, a feeling of unease persists.

Perhaps the first source of discomfort is the fact that offshore Chinese property bonds are deeply subordinated, since they are issued by offshore-incorporated entities, which inject the bond proceeds as equity into their onshore companies and service their debt only out of equity dividends received back from the mainland. The difficulties in repatriating equity funds out of China mean that the offshore principal effectively has to be refinanced. In case of bankruptcy, the onshore lenders have the first claim over the onshore assets.

While this structural weakness is undoubtedly true, it applies to every other bond issued by Chinese businesses, including investment-grade bonds far beyond the property sector, since the structure was born out of regulations prohibiting the issuance of debt or guarantees by mainland companies. (Only recently have the authorities begun to relax this prohibition, and the first few offshore bonds are now coming out with direct guarantees from mainland operating companies.)

ANOTHER SOURCE OF discomfort is the government’s meddling in the property sector through various measures, including the flow of credit to the builders, rules for financing land purchases, obtaining mortgages, and mortgage down-payment requirements. The harshest controls came in 2010 when the government restricted the number of apartments that an individual could purchase.

Property prices are a sensitive subject everywhere, and China is no exception. The government presses the brakes if the prices are speeding too fast and pushes the accelerator if property construction flags too much so as to threaten the overall economic growth.

This government intervention makes asset values volatile in both equity and debt markets, and raises the cost of capital to the sector.

Some investors have also been scared away by stories of oversupply and ghost cities. The property development business model, by definition, consists of a long operating cycle, and there may be genuine demand/supply imbalances, as in any other industry, but the overwhelming majority of Chinese properties are built in response to actual demand from a rapidly urbanising population. The same goes for talk of speculative buying, when the reality is that most of the properties are bought for self-occupation. Buyers have to put up a minimum 30% down-payment, they are not over-leveraged and there is no subprime lending.

WHEN IT COMES to investing in Chinese property bonds, one should realise that there has already been one level of filtering – only those companies large enough to go through a rating process and the expense of issuing offshore actually end up selling dollar bonds. They are all listed offshore, most of them in Hong Kong, and are subject to audits and disclosures that go with the listing status. The additional scrutiny from equity analysts and investors that comes with listing also offers additional information for bond investors.

There has not been a single default in the sector so far, and only two distressed exchanges in 2009, both at 80 cents to the dollar. Some companies did go through financial distress during previous sector downturns, but they managed to sell land or unfinished projects to stronger players and stave off default.

This is not to argue that we would never see a default in the sector. We will, sooner or later. But the sector has genuine fundamentals, strong and weak players, and saleable assets that can be realised in times of distress.

So, how should one approach investments in Chinese property bonds? First of all, investors need to be prepared for the volatility that comes with the regulatory changes. Any crash in value following a regulatory tightening offers an opportunity to pick up the higher-quality bonds at more attractive prices. In fact, such moves also enable the stronger players to buy out the weaker ones or to acquire assets from the struggling players, and increase their market share.

The current downturn in the market is no different. It is true that the stock of unsold property is running above average; that the leverage has increased in the last 12-18 months in response to slowing sales; that margins are under pressure due to the pressure to liquidate stock; and that some of the weaker companies are likely to experience a liquidity crunch in the next 12-18 months, unless they slow down their expansion. But the current downturn is also an opportunity to pick up bonds issued by stronger companies, which will benefit from the tight conditions in the sector. The challenge is reading the credit fundamentals carefully enough to identify the winners.

RSS Feed

RSS Feed